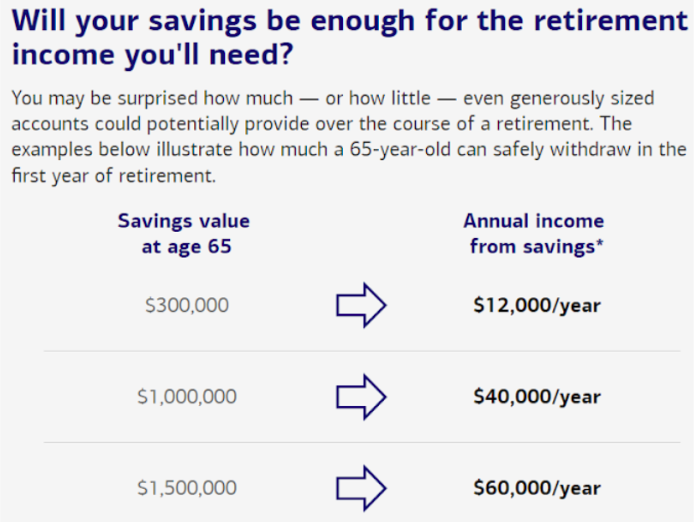

It is impossible to determine a general minimum amount that would work for everyone in retirement, everyone is unique and different. The answer is, it depends on the lifestyle you plan to live. For some people $1 million in retirement savings is plenty. For others who receive a significant pension, $200k is plenty. This depends on a few factors, like your lifestyle, expected expenses, and how long you plan to be retired for. Another important factor is your sources of income; Social Security, pension, RMD’s, real estate, annuities will determine the shortfall in your income and determine how much of your portfolio you will need to withdraw.

Source: Chief Investment Office, March 2024 (PDF). Illustration is for hypothetical purposes only.

The size of your nest egg and how long it will last, depends not just on how much you save and invest, but primarily on how you plan to spend your time during retirement. Will you work part-time? Do you dream of traveling frequently? And at what age do you plan to retire? These are key questions to help determine how much you’ll need to ensure the lifestyle you want. It’s also important to keep inflation and future market conditions in mind when planning. By planning for these factors early, you’ll be better prepared to create a nest egg that can comfortably support your retirement goals.

Taxes can significantly impact your retirement savings as well. Contributing to a pre-tax account like a traditional 401(k) differs from saving in a Roth IRA, which is funded with after-tax dollars. The key difference lies in how these accounts are taxed when you withdraw the money in retirement. A Roth Conversion could be a good solution and understanding the timing of when to convert could save you a good amount in taxes.

- Calculate Future Expenses:

Setting a specific savings goal, whether it’s a percentage or a dollar amount, can be a good place to start. Everyone’s lifestyle and retirement spending habits are different so estimating an annual budget based on your current expenses and considering how they might change in retirement is a good idea.

Keep in mind, while some things—like healthcare and inflation—may rise, there could be savings in other areas. Research shows that retirees often spend more time bargain shopping and cooking at home, which can lower everyday living expenses.

A study by the RAND Corporation found that overall spending tends to decrease as people move through retirement, though the breakdown shifts. For instance, healthcare costs for higher-income retirees rise from 9-10% of household budgets at ages 65-69 to 14% after age 80. Meanwhile, travel spending drops from around 8% in their 60s to about 4% in their 80s. Understanding these changes can help you better anticipate and plan for your future expenses.

2. Add Up All Potential Income Sources

As you consider how much you’ll need in retirement, keep in mind that your savings and investments are just one piece of the puzzle. For most Americans, Social Security (along with some remaining pensions) will be the foundation of their retirement income. Even if benefits are reduced in the future, Social Security isn’t likely to disappear entirely.

Beyond that, remember to factor in other potential income sources that could support you in retirement. These may include funds from your workplace and personal retirement accounts, and annuities. Annuities can act as a replacement to your pension and can be a reliable source of retirement income. Fixed income annuities can function as both retirement savings and retirement income. With several different payout options, which can include creating a steady income stream based off you or your partners lifetime– annuitization or a lumpsum.

Conclusion

Understanding your post-retirement expenses and projected income is key to estimating how much you’ll need to withdraw from your savings each year. However, it can be challenging to translate that long-term goal into a specific amount to invest today, especially if retirement is still decades away. To get a clearer picture of where you stand now and what adjustments you might need to make, try using the Personal Retirement Calculator. This tool projects your savings and helps identify any gaps between what you’re on track to have and what you may need. With these insights, you can refine your strategy and make sure you’re prepared for the future. Check out Smart Asset’s Retirement calculator